Getting GST 2.0 to Run Like a Well-Oiled Machine

Historic Reform in Indirect Taxation

- At the 56th GST Council meeting (Sept 3, 2025), landmark reforms termed GST 2.0 were approved.

- The reform simplifies India’s indirect tax system, with major implications for consumers, MSMEs, industry, and the wider economy.

Simplified Rate Structure

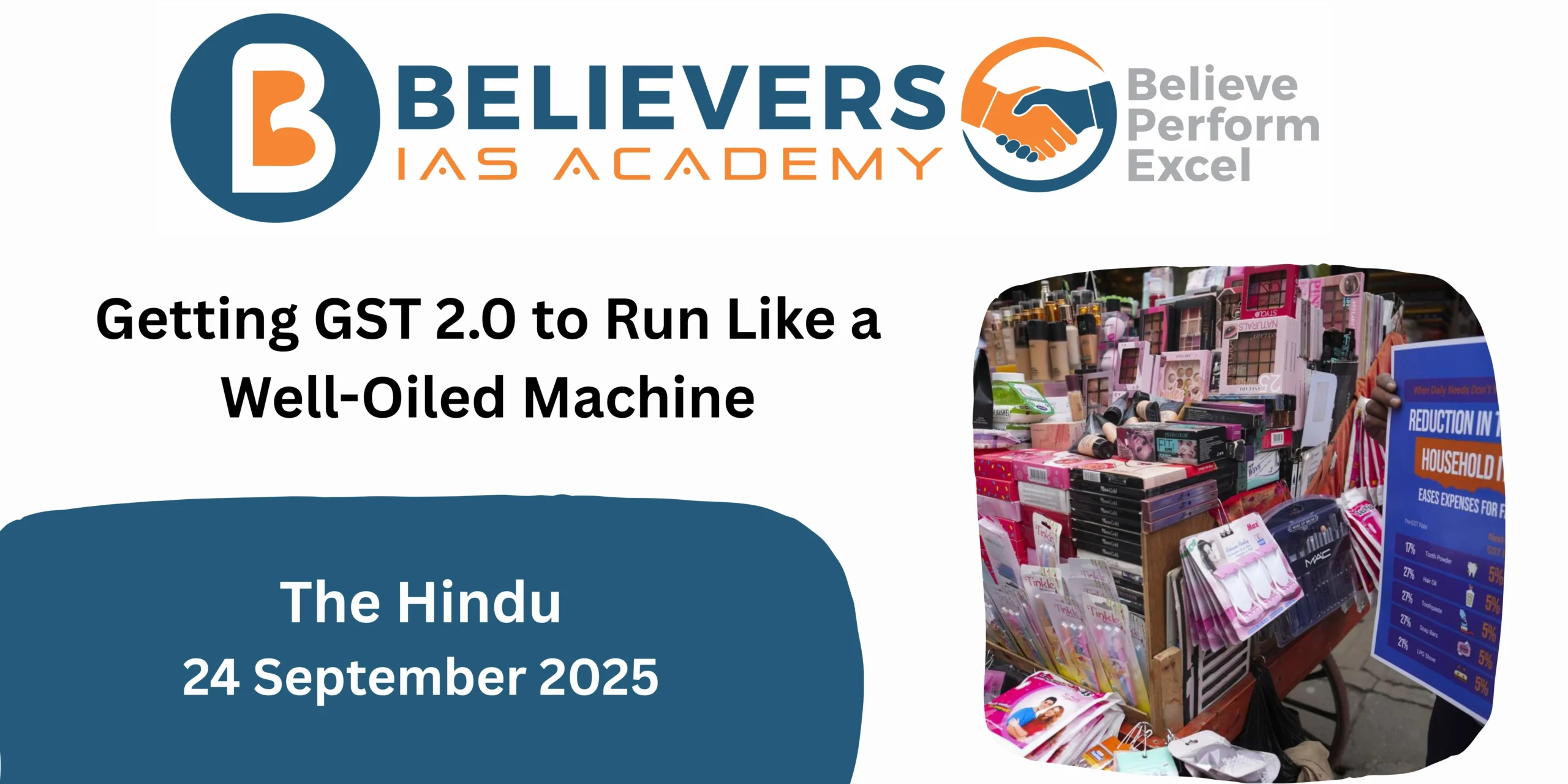

- Old four-slab system (5%, 12%, 18%, 28%) replaced with:

- ~5% for essentials.

- 18% as the standard rate.

- 40% for luxury and sin goods.

- Over 99% of goods and services now fall under 0%, 5%, or 18%, with only 1% in the highest category.

- Daily-use goods such as toiletries, small appliances, FMCG items shifted to lower slabs.

Consumer Benefits

- Direct and visible savings for households, especially middle- and lower-income groups.

- Expected to moderate inflation, as many goods that were taxed at 12–18% now attract 5% or less.

Gains for Industry and MSMEs

- Lower input costs and reduced litigation.

- Simpler compliance norms: stock adjustments without full relabelling, faster refunds, clearer classification.

- Relief for sectors previously hit by inverted duties: FMCG, textiles, small vehicles, cement, farm equipment.

- Several companies, including public sector insurers, pledged to pass on savings to consumers.

CII’s Role in Advocacy and Transition

- Since Dec 2024, CII has been pushing for rate rationalisation, classification clarity, and reduced compliance burdens.

- Post-reform, CII is conducting awareness sessions nationwide to help firms—especially MSMEs—adapt.

- Engagement with authorities on labelling, packaging, and transition of stocks to ensure smooth rollout.

Economic Impact

- Expected to boost consumption, especially in rural/semi-urban areas where price sensitivity is high.

- Inflation moderation in key consumption items.

- MSMEs to benefit from improved margins and working capital.

- Analysts project an additional 1% GDP growth through higher demand.

- Short-term revenue loss for Centre and States (tens of thousands of crores), but likely offset by:

- Greater consumption.

- Better compliance.

- Formalisation of economy.

- Long-term fiscal buoyancy.

Implementation Challenges

- Ensure that tax cuts benefit end-consumers, not captured in supply chains.

- Strengthen administrative systems: GSTN, State tax departments, metrology, labelling authorities.

- Special support for MSMEs with limited resources for compliance.

- Need for feedback loops to address classification confusion, unsold stock, and packaging issues.

Conclusion: A Defining Reform

- GST 2.0 is a structural transformation, not just a tax cut.

- Success depends on trust and cooperation between government, industry, and consumers.

- CII commits to capacity-building, advocacy, and ensuring ground-level success so that GST 2.0 delivers its full promise.

Related Posts